When the Chips are Down

An interview with Chris Miller, author of Chip War: The Fight for the World's Most Critical Technology

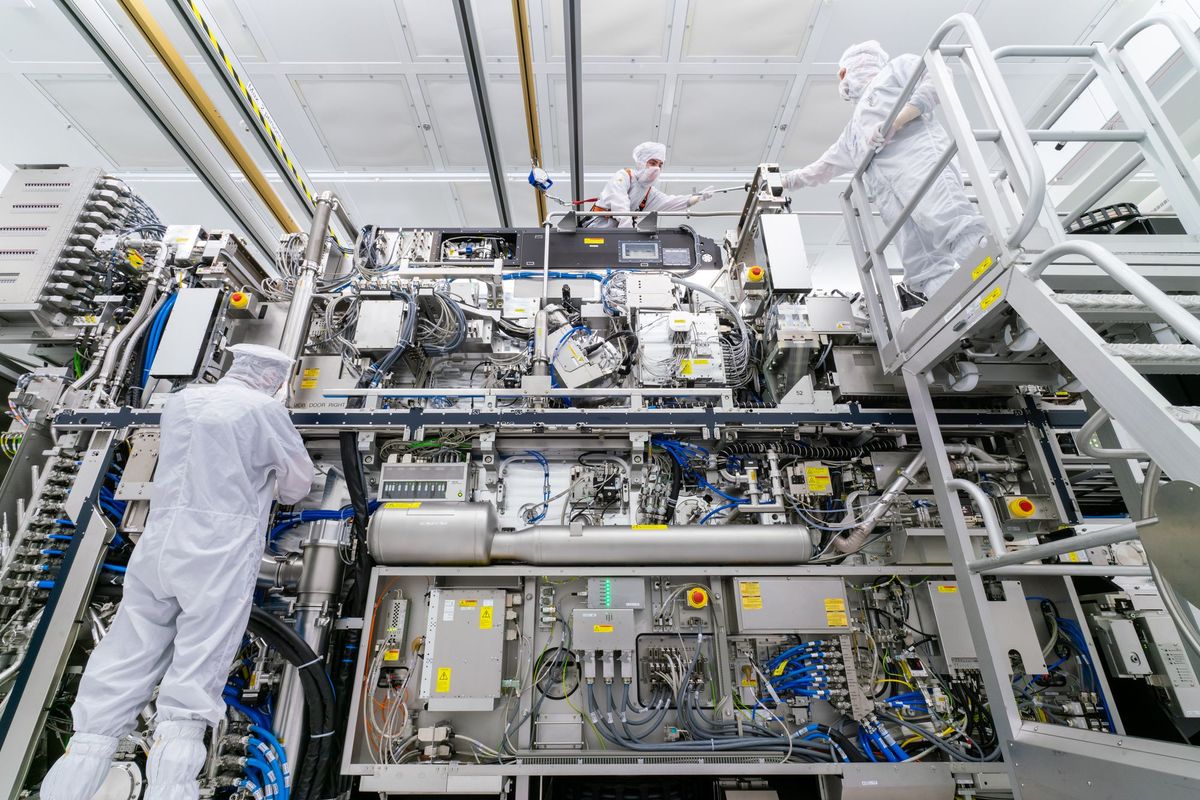

In the 75 years since the transistor was invented at Bell Labs, semiconductors have reshaped computation, communication, and global power structures. Today, microchips are packed with a dizzying number of transistors – as Chris Miller explains, “Last year, the chip industry produced more transistors than the combined quantity of all goods produced by all other companies, in all other industries, in all human history. Nothing else comes close.” Producing ever more precise and powerful chips has led to massive consolidation in the semiconductor industry and a whole host of geopolitical conflicts.

In Chip War: The Fight for the World's Most Critical Technology, Chris Miller chronicles the history of invention and the decades-long rivalries and collaborations that shaped the industry. He provides shrewd insight into the current tensions and export controls around semiconductors that are reshaping the US and China’s relationship. Chris is an economic historian and associate professor of international history at Tufts University. He recently joined Scope of Work's Member’s Reading Group for a conversation about the shifting global powers in semiconductor fabrication. What follows is an edited and condensed transcript of our discussion.

Hillary Predko: There are interesting parallels between the Cold War and America’s rivalry with China today. The US really dominated semiconductors during the Cold War and used that advantage as a lever to outpace the Soviets technologically. However, many things have changed – today there are so many choke points in the industry and fewer fabs in the US. Do you think that export controls can be an effective lever against China's chip industry at this moment?

Chris Miller: Well, I think the reason why it's been hard to catch up with the cutting edge is primarily that the chip industry moves so rapidly. That's been true regardless of the export control context. In an industry where you've got Moore's Law dynamics doubling every two years, that's a faster rate of improvement than basically any other segment of the economy ever. The fact that the race is so rapid means that catching up is really hard.

There are examples from the Cold War where export controls made it even harder to catch up – the US was racing forward and the Soviet Union was unable to get a lot of the tools that it needed to make chips efficiently. They could smuggle some of them in but had to deal with making spare parts, had to wait for spare parts, and didn't have the know-how to use the machines properly. That's where China finds itself today. Now, there are a million differences between China and the Soviet Union that we could go into, but I think there's a basic similarity. Today China's still a relatively small player in the world chip industry and growing rapidly, but still small at the cutting edge. When it comes to cutting edge tools, they're largely produced by a small number of companies in a small number of countries.

China's no doubt going to try to find ways to get around them and will make some progress. We shouldn’t measure the efficacy of controls by whether they stop Chinese progress – they're not going to do that – but whether they slow it down. However, that's a hard thing to measure because you don't know what speed China would make progress at in the absence of export controls. I completely suspect that in 10 years, people will look back at the export controls and disagree on what impact they had, because we won't be able to know their impact objectively relative to the non-export controlled trajectory.

James Coleman: On the flip side, what's the potential of the CHIPS Act to spur US domestic manufacturing? And how does that compare with how other countries are investing in their semiconductor industries?

CM: So if you look at the history of the industry, you'll find most governments have invested. In the US it's mostly been about government-backed R&D and procurement of chips for the defense industrial base. In other countries, there's been much more direct subsidization of manufacturing capacity, which the US hasn't really done. And because other countries have put more into financing the build-out of manufacturing capacity, there's been more manufacturing capacity built outside the United States. That's not a surprise, it's just basic economics.

The CHIPS Act is intended to change that. First, the legislation sets out funds to provide incentives for manufacturing. It's not a surprise that we've already gotten a big increase in chip making facility construction in response to that act – that's easy and understandable. We shouldn't be surprised that when the government hands out money, people respond by building out more capacity. But we also shouldn't assume that will continue forever because the government's not going to want to spend this money forever.

I think that the key question is: Will we get second-order effects of the money that's spent that induce companies to build more capacity – not just now, but in two years, four years, and six years? Will these companies build up facilities that operate productively, and become integrated into broader ecosystems? The success or failure of the act will be judged by whether it delivers these long run effects beyond the expenditure of the initial $39 billion.

HP: Yeah, that's a big ship to turn around. I was amazed to learn how early semiconductor fabrication started globalizing – you mentioned in the book that US firms started outsourcing in 1963.